Available for professional engagements & collaborations

BERTIN

BALOUKI SIMYELI

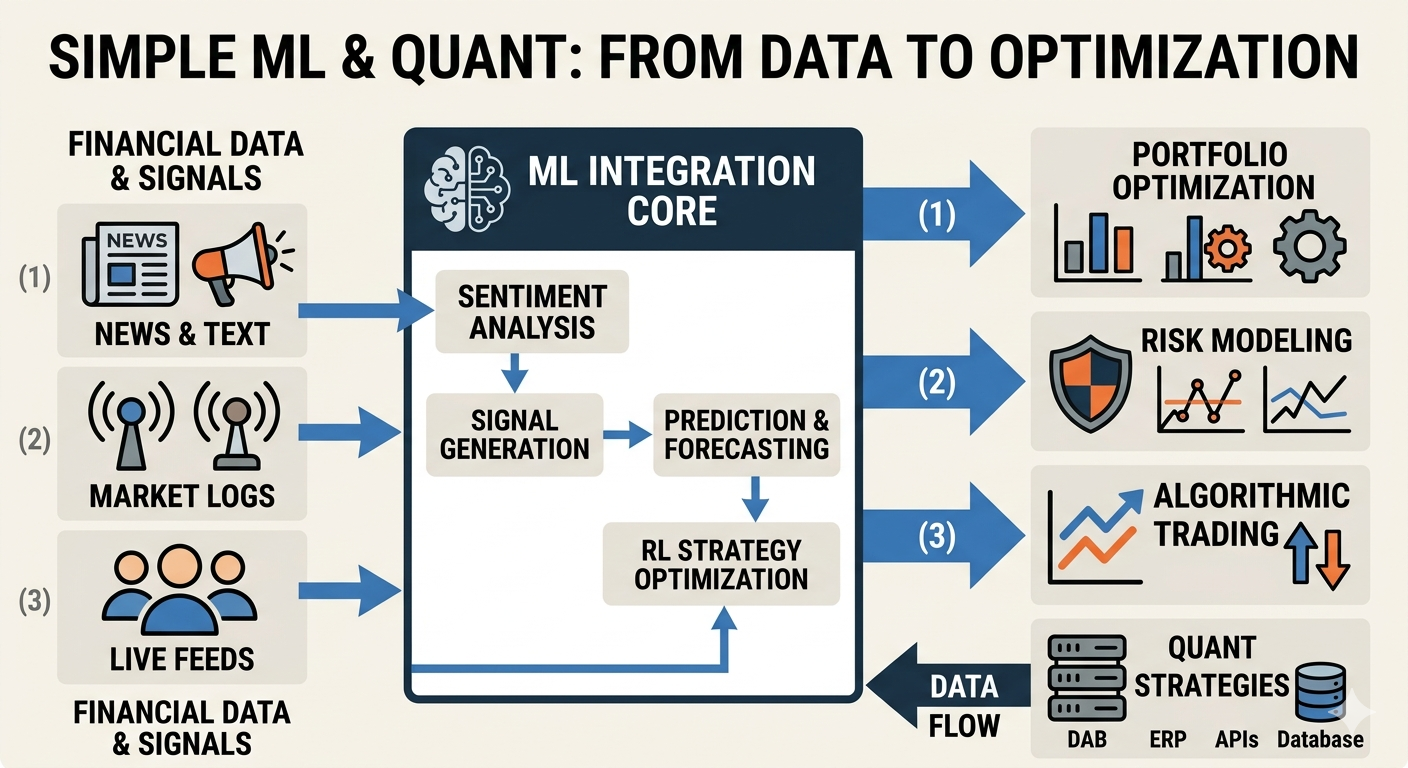

Building high-performance trading infrastructure and intelligent AI systems at the intersection of financial markets, low-latency computing, and large language models. CTO at two companies. Open-source author with 70k+ downloads. $56M+ in trading volume.

Python 3.12+

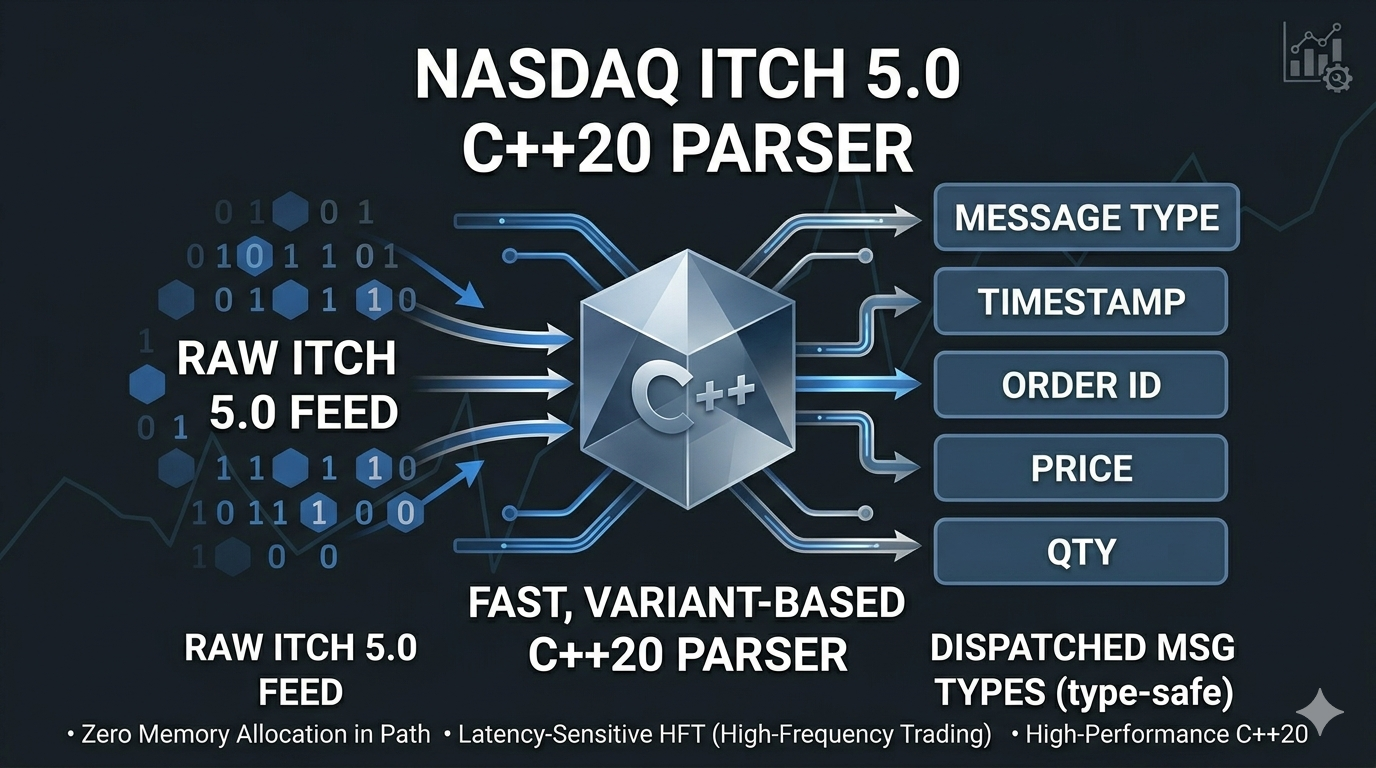

C++20

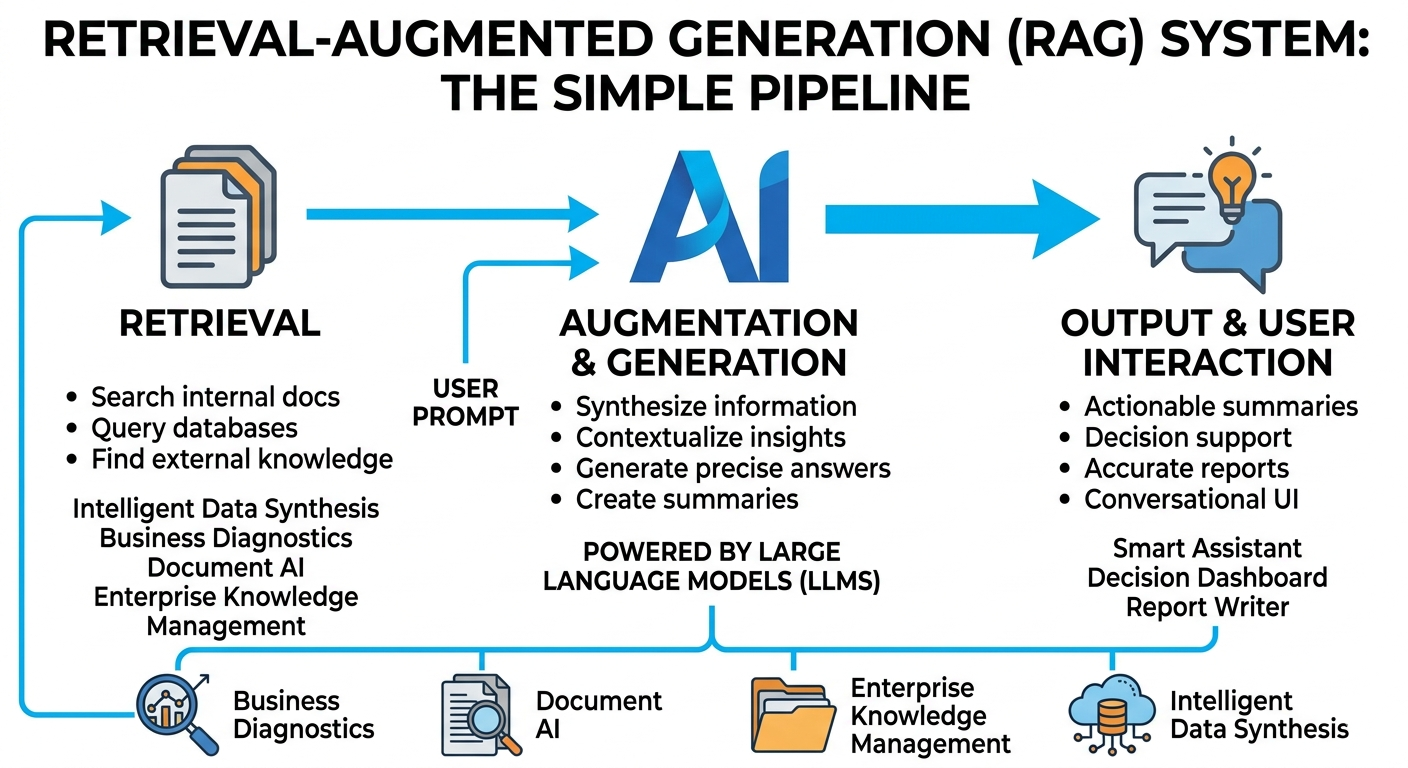

LlamaIndex

RAG Systems

Gemini API

MetaTrader 5

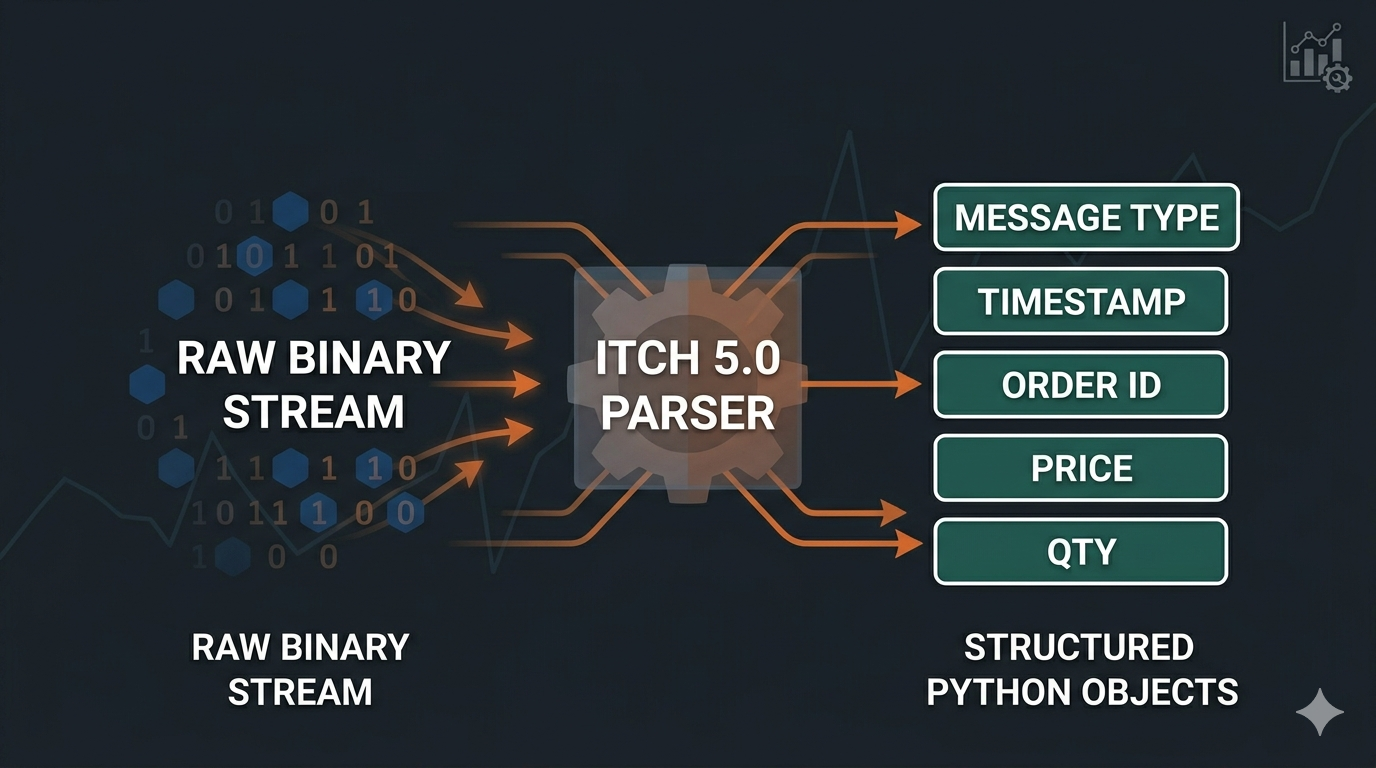

Nasdaq ITCH 5.0

HFT Systems

Harvard CS50x

West Africa 🌍

bertin@bbs-ai ~

pip show bbstrader

Name: bbstrader

Summary: Investment & Trading

Toolkit, Python & C++

Author: Bertin Balouki

SIMYELI

bertin@bbs-ai ~

python -c "from llama_index.core import

VectorStoreIndex"

🤖 AI Stack

📦 PyPI Downloads

70k+

bbstrader · itchfeed

📈 Trading Volume

$56M+

JustMarkets · 316 lots

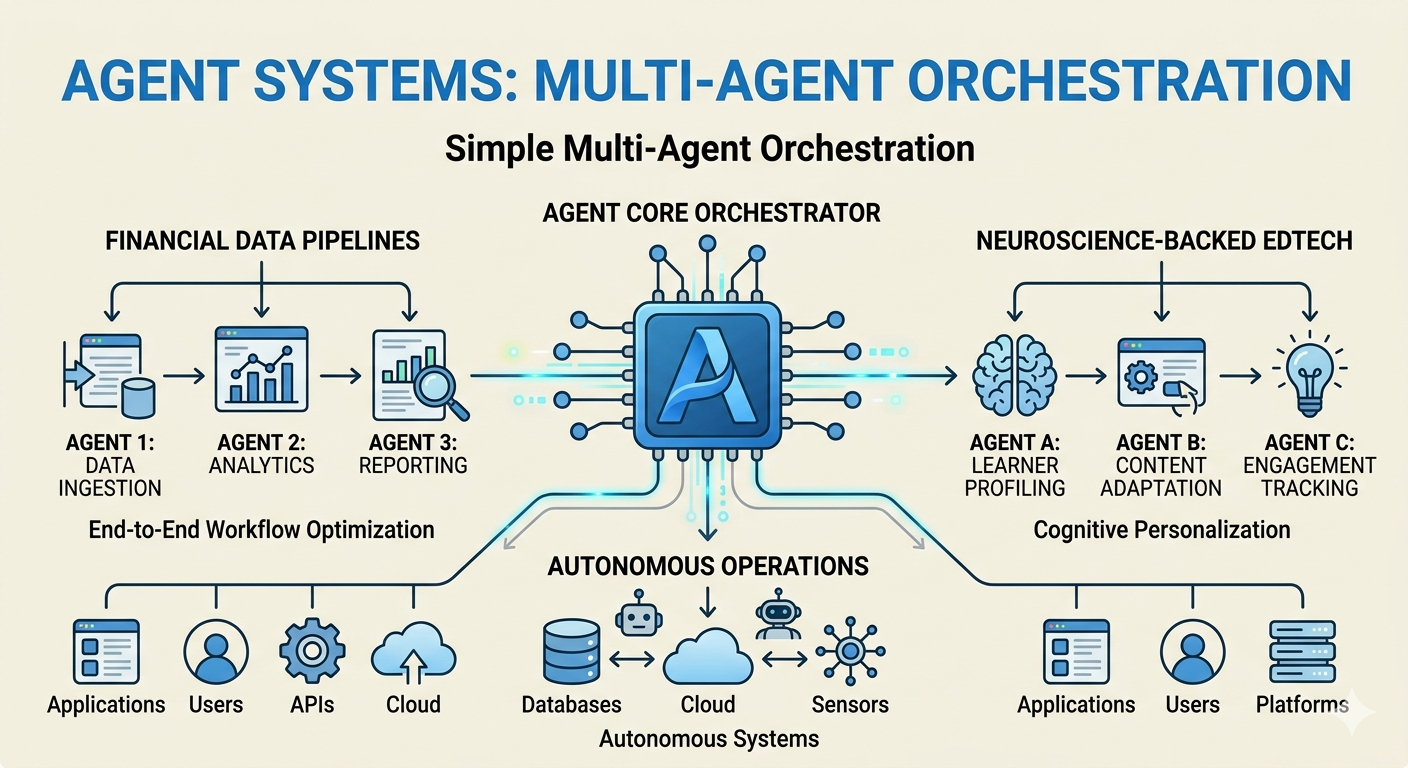

🏛️ Leadership

2x CTO

Movable Games · Forward Outlook